Overview of the Swiss system

The depositor protection system is designed to prevent banks from becoming bankrupt. If a bank were to become bankrupt, clients could lose at least part of their deposits.

Depositor protection

Depositor protection in Switzerland is made up of the following key elements:

- Regulation

legislators have laid down strict conditions that banks must meet in order to accept client deposits. For example, banks must hold sufficient capital and liquidity to be able to pay out their client deposits at any time. There are also rules about how banks must be organised. - Supervision

the Swiss Financial Market Supervisory Authority FINMA supervises banks on an ongoing basis to ensure that they comply with these strict rules. If a bank gets into financial difficulty, FINMA can order protective measures or restructuring measures to avert bankruptcy. - System stability

the Swiss National Bank (SNB) can take measures to maintain the stability of the financial system. - Deposit insurance

the deposit insurance scheme is activated if a bank nevertheless becomes bankrupt. In the event of a bank’s bankruptcy, the deposit insurance scheme protects client deposits against loss up to the amount of CHF 100 000.

Who or what is a depositor?

Depositors are clients who hold a credit balance in an account with a bank.

What is depositor protection?

The term ‘depositor protection’ encompasses all the elements that contribute to protecting clients of banks in Switzerland and thus strengthen the country’s stability as a financial centre.

What is desposit insurance?

Deposit insurance is one element of depositor protection in Switzerland. In the event of a bank’s bankruptcy, the deposit insurance scheme protects client deposits against loss up to the amount of CHF 100 000.

Deposit insurance

The deposit insurance scheme consists of the following key elements:

- All banks must hold collateral consisting of assets in Switzerland equivalent to 125% of the protected and preferential client deposits.

- Protected deposits have preferential status in the event of bankruptcy.

- The bank’s liquidator appointed by FINMA uses the bank’s available liquidity to pay out the protected deposits.

- esisuisse funds the payment for the protected deposits if the bank has insufficient liquidity available. The banks make a maximum of CHF 7.9 billion available to esisuisse for this purpose.

This amount corresponds to the value specified in the law of 1.6% of all protected deposits in Switzerland.

The banks must provide esisuisse with collateral (securities or money) for half of these approximately CHF 7.9 billion by 01.12.2023 at the latest.

What are deposits?

Deposits are client balances on accounts held at banks.

Who is classed as a client?

All clients (private and corporate) of banks are protected by deposit insurance scheme: Natural persons (adults, children) and legal entities.

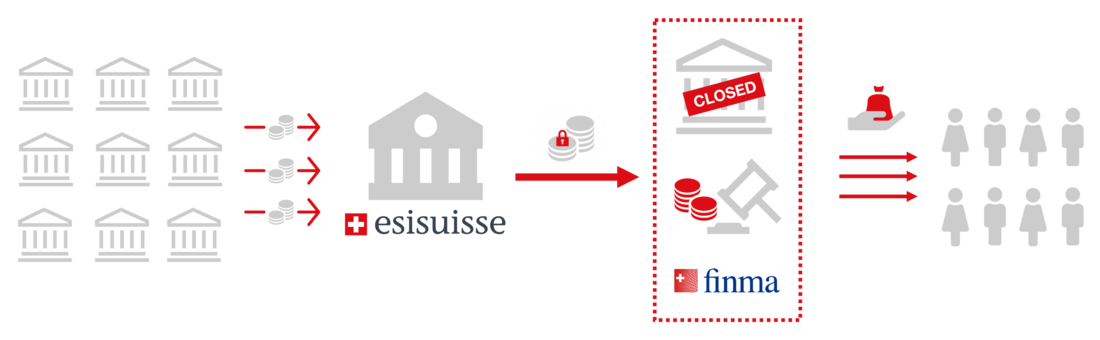

Bankruptcy of a bank

- The liquidator first uses the bank’s available liquidity to pay out the protected deposits.

- esisuisse must finance the payout of the protected deposits if the bank’s liquidity is insufficient.

- Only in this unlikely scenario does esisuisse make the necessary funds available to the liquidator.

- esisuisse may collect this additional money at any time from all other banks.

- The liquidator pays out the protected deposits to the affected clients.

Are my pension assets also protected by esisuisse?

No, balances in vested benefits or Pillar 3a accounts are not covered by the deposit insurance scheme, but they are treated as preferential up to a maximum of CHF 100 000.

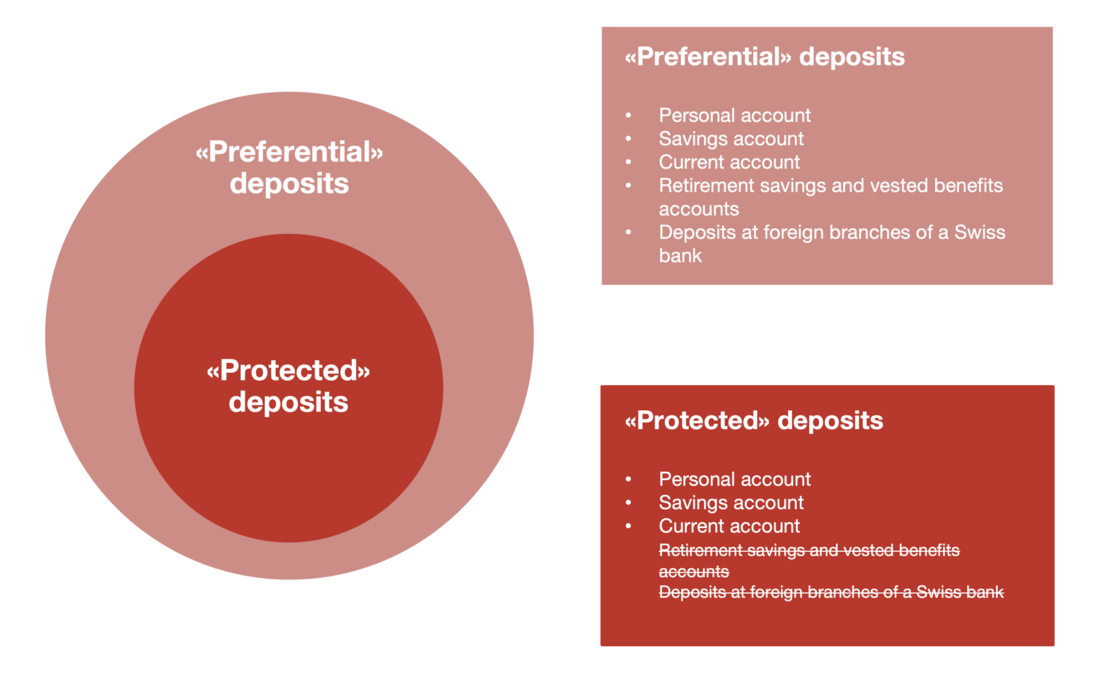

What is the difference between «preferential» deposits and «protected» deposits?

Preferential and protected do not mean the same thing. Preferential is primarily a question of bankruptcy law. It means that the deposits fall into the second creditor class rather than the third.

Protected deposits are a category of preferential deposits that have additional protection under the deposit insurance scheme, and that can be paid out.

Preferential deposits are not normally paid out until in the course of or at the end of the liquidation procedure.

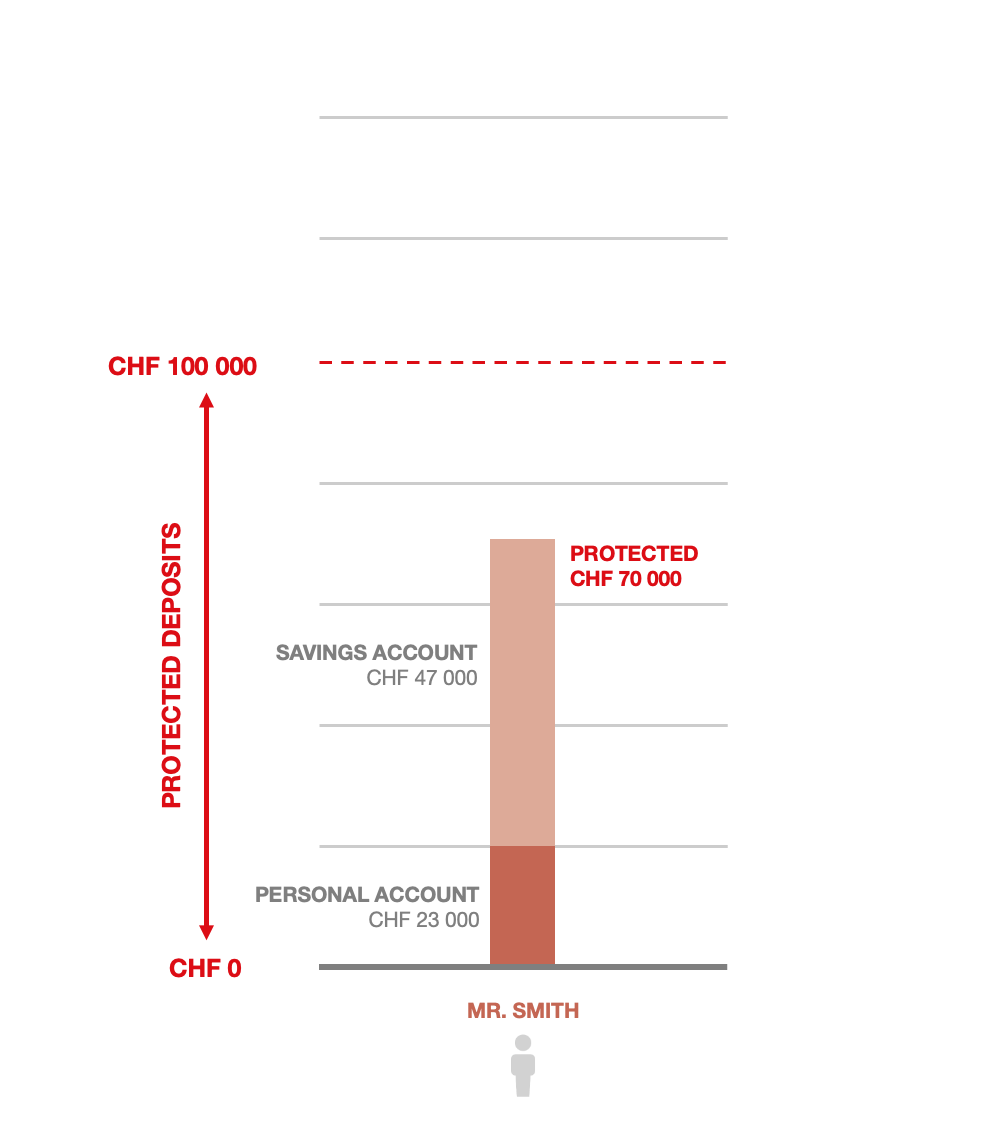

Example 1: Individual with assets < CHF 100 000

Mr. Smith has a personal account with a balance of CHF 23 000 and a savings account with a balance of CHF 47 000 at the bank.

In the event of the bank’s bankruptcy, Mr. Smith will be paid out the entire total of CHF 70 000 via the deposit insurance scheme.

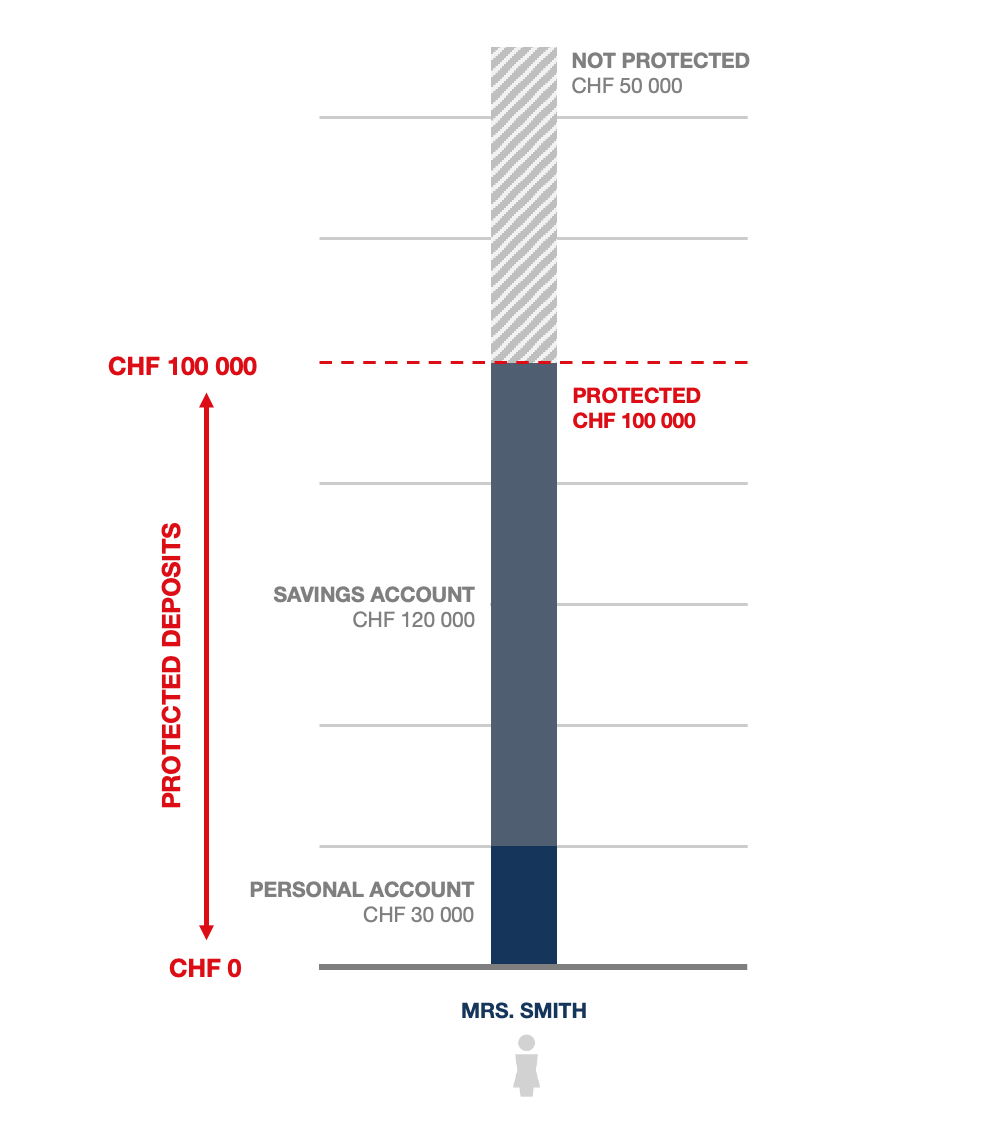

Example 2: Individual with assets > CHF 100 000

Mrs. Smith has a personal account with a balance of CHF 30 000 and a savings account with a balance of CHF 120 000 at the bank.

In the event of the bank’s bankruptcy, Mrs. Smith will receive a payout of CHF 100 000. The remaining CHF 50 000 is not covered by the deposit insurance scheme. It is assigned to the third creditor class, and Mrs. Smith will be paid out at least part of the amount once the liquidation has been completed.

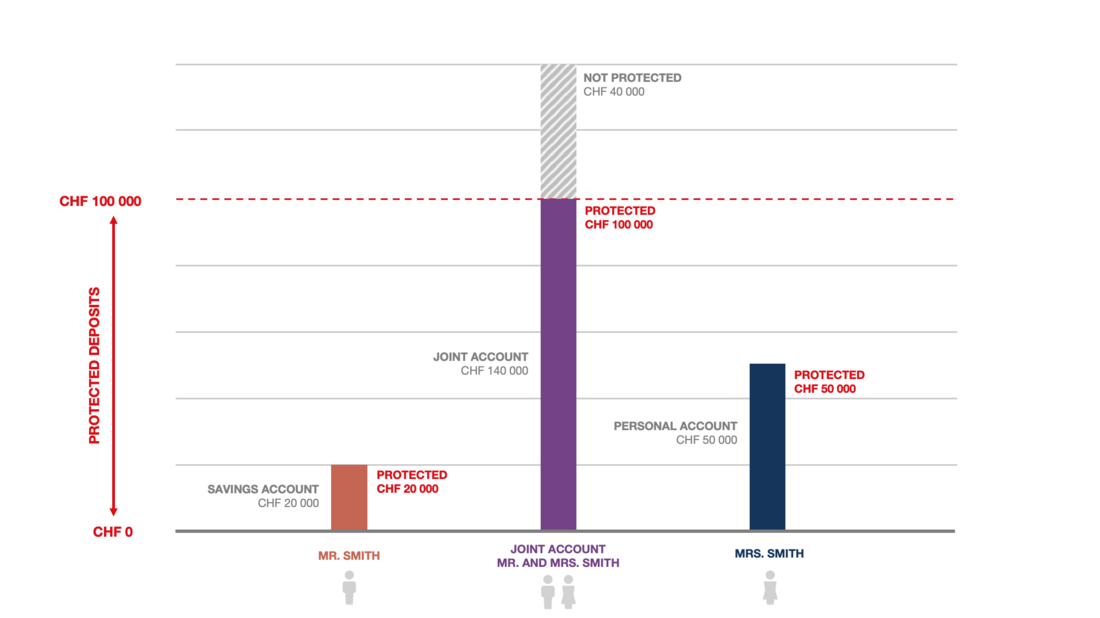

Example 3: Couple with a joint account

Mr. and Mrs. Smith have a joint account with a credit balance of CHF 140 000. Mrs. Smith also has a personal account with a credit balance of CHF 50 000. Mr. Smith also has a savings account with a credit balance of CHF 20 000. All the accounts are held at the same bank.

Mr. and Mrs. Smith have a protected deposit of CHF 100 000 as a group from the joint account. The «surplus» share of CHF 40 000 falls into the third creditor class. «Surplus» amounts cannot be transferred to the other spouse or other persons.

Mrs. Smith's credit balance of CHF 50 000 and Mr. Smith's credit balance of CHF 20 000 are also fully protected.

The insurance in this example totals CHF 170 000.

Is my money that I hold at my bank protected?

Deposits at banks that operate a branch in Switzerland authorised by the Swiss Financial Market Supervisory Authority FINMA are covered by the deposit insurance scheme. This includes the cantonal banks and PostFinance. Only deposits at securities firms authorised by FINMA as «account-holding» are covered by the deposit insurance scheme.